If you work a 9-5 job, then I believe you will really understand how difficult it is to find time for other businesses. Maybe you’ve finally succeeded in starting a business but finding a balance with the 9-5 job becomes a daunting one.

Don’t Worry, I will be sharing with you 5 success tips on how to escape the grind of 9-5 jobs and be the boss of your own.

Let’s get started:

Tip 1: Have A Definition Of The Business You Want[ps2id id=’Have-A-Definition-Of-What-You-Want’ target=”/]

I know you want: To be your own boss, Make more money and have more freedom.

That’s everybody’s dream, But is that what you really want?

If yes, then

Have you define it: I mean the business that you want to start.

Often times our definition of the business we want centers around our passion. Passion is great, but it needs to be channeled into achievable goals.

That’s where the need to have a definition of the business you want comes in.

In order to succeed in business, you need to know the business you want, understand what it will take to get there and then execute a plan in order to arrive at your business goals.

Here are a few steps to help you come up with a better definition of the business you want:

- Sit down and make a list of all the business ideas you had.

- Make a research of the niche you have chosen.

- Find a mentor.

- Identify the expertise and resources required.

Tip 2: Create Your Business Master Plan[ps2id id=’Create-Your-Business-Master-Plan’ target=”/]

You’ve already defined the business you want, right.

The next step is to create your business master plan. What you really need here is to have an understanding of what your business goals are and the strategy for achieving them.

Don’t get down with the traditional “business plan” format and requirements. But create a more realistic, feasible and tangible business plan.

The type that will be your guide.

Here are three quick steps that will help you come up with a better business master plan:

1. State Your Services, Products or Offer

To succeed as an entrepreneur, you must carefully choose your services, products or offer correctly. More than any other factor, your ability to make this choice will determine your success or failure.

So how do you start?

First, start with a self-analysis:

- What kind of products or services do you like, enjoy, consume and benefit from?

- Do you like the product or service you’re planning to sell?

- Can you see yourself getting excited about this product or service?

- Would you buy it and use it yourself?

- Would you sell it to your mother, your best friend, your next-door neighbor?

- Can you see yourself selling this product or service for the next five to 10 years?

- Is this a product or service that you intensely desire to bring to the marketplace?

Second is the customer’s analysis:

- What does the product achieve, avoid or preserve for the customer?

- How does the product improve your customer’s life or work?

- What kind of customers will you be selling the product to?

- Do you personally like the customers who’ll be buying this product or service?

Last, is product analysis:

- Is there a real demand for the product in the market and at the price you’ll have to charge?

- Is the demand large enough for you to make a profit?

- Is the demand concentrated enough so you can advertise, sell and deliver the product at a reasonable expense?

For a product or service to succeed, it must be the right product or services, being sold at the right time, to the right customer, in the right market.

It must be produced and sold by the right company, and the right people.

What you have to decide is this: Is this product, service or offer right for you and your customers.

Answering this question will help you with a better idea of your product, services and offers will be.

2. Identify Your Niche (Target Market)

You have finally gotten that killer product, services or offer, but your work is not yet done.now you need to identify your target market to know whom and where your product or service is satisfying.

So what do you do?

One of the most effective things you can do for your product, service or offer is to have a good selling position i.e. to narrow your gaze and identify your niche.

I mean bring your niche to a focus.

As an example; Imagine you are a local coffee seller interested in marketing services.

Who would you rather hire?

Applicant Y: “I help businesses skyrocket their marketing”

Applicant Z: “I help coffee sellers improve their marketing”

Since one person focuses only on your type of business, you will have a lot more trust in his expertise to improve your marketing actions because his expertise is specific to your type of business than the other.

Won’t You?

So you would rather go for applicant Z.

That’s the importance of identifying your niche or the targeted market for your business.

3. Develop A Value Proposition

Once you have stated your services, products or offer, and identify your niche (target market), the next thing is to develop a value proposition.

Your value proposition is your business positioning statement that explains what benefits your business provides for who and how you do it uniquely well.

Here are a few steps that will help you come up with a better value proposition:

- State the problem clearly: Is the problem solvable? even if it is solvable, is it undeserved? No, it is underserved, then Is it avoidable? If not, is it urgent?

- Qualify the problem: Is it BLAC; Blatant, Latent, Aspirational, Critical? if yes, does it indicates a recess in the market, allowing you to capitalize on the niche?

- Evaluate your solutions: You have stated and qualified for the problem. Finally, you’ve got the answers to the problem. what’s next? should you go ahead to solve the problem?

But wait! you need to evaluate your solutions.

Ask yourself: What is unique and compelling about your solution?

Do not lose sight of the fact that you are core to your venture’s value proposition.

What problems do you understand uniquely well? What solution can you deliver uniquely well? What kind of disruptive business model can you bring?

Be true to yourself and you will go far.

Tip 3: Map Out Your Finance[ps2id id=’map-out-your-finance’ target=”/]

Your business master plan may not mean anything to you if you can’t justify it with a good figure. I mean mapping out your finance.

Mapping out your finance is one of the most essential components of the business master plan, as you will need it if you have any hope of winning over investors or obtaining a bank loan.

Even if you don’t need an investor or bank loans, it’s important you map out your financial plan in order to know your financial strength.

You do this in a distinct section of your business plan. The trick is to underestimate revenue and overestimate expenses.

Here two steps to come up with a more realistic map for your business plan:

1. Make A Realistic Startup Budget

The rule of thumb when filling in the numbers in the financial section of your business plan, is to start with a startup budget. For planning purposes, it is advised you define your budget in terms of startup expenses ( expenses you incur before launching the business) and assets ( which may includes cash in the form of the money in the bank when the company starts), and in many cases, starting inventory.

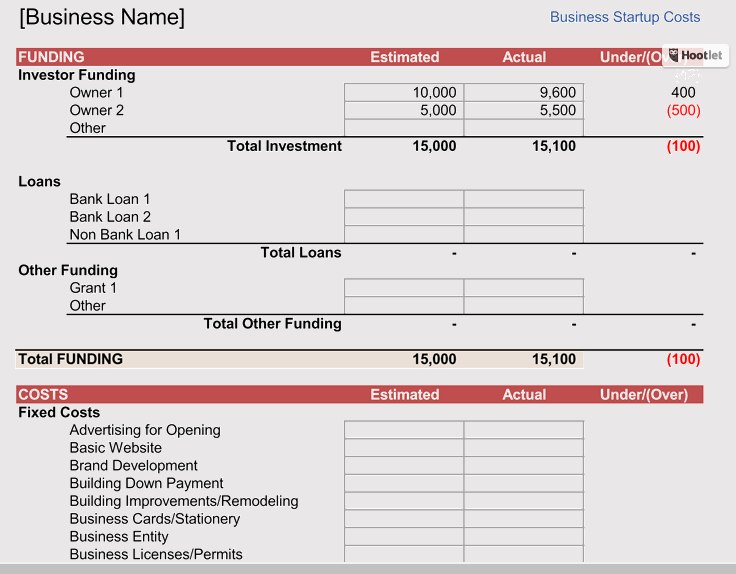

2. Set Up A Startup Cost Worksheet

Your startup cost worksheet should answer what the money is going for: Make sure you have included every cost. It is better to over-estimate so that you don’t get short with the money you receive from your loan.

Once you understand all of the cost categories involved, you verify to ensure that your plan has captured all of the expenses needed to get started.

You can use a worksheet in a spreadsheet application like Microsoft Excel to Set up the Startup-Costs worksheet like the one shown below.

- Office equipment and furniture for owners and employees

- Specialized equipment for manufacture, warehousing, or shipment of products

- Computers, software, and peripherals (printers, etc.) for office and other areas

- Phone systems, cell phones, and computer networking equipment

Depending on your business, you may need to lease or buy vehicles for:

- Delivery

- Manufacturing activities

- Cars for salespeople

- Cars for executives

– Business Supplies and Advertising Materials: Include the following basics on your supplies list:

- Office supplies

- Janitorial supplies

- Supplies for manufacturing activities

- Supplies for shipping and mailing

- Stationery and business cards

- Advertising materials, such as brochures, flyers, other printed advertising material

- Costs for an advertising agency to prepare an ad campaign for your startup

- Design costs for advertising and web site

- Website setup

– Other Startup Costs: You’ll need to include funds to cover certain administrative costs for necessary startup tasks:

- Fees for attorney to set up legal ground for your business, to assist with commercial lease documents, and other pre-startup negotiations

- Fees for CPA to set up a bookkeeping system

- Local business licenses and permits

- Insurance deposits

There may be other costs you didn’t expect, so include a comfortable amount as a buffer for any other miscellaneous expenses that might come up.

– Putting it All Together:

Calculate the subtotals for each section above and create a grand total start-up costs statement. If you are contributing equipment, vehicles or other startup items to the business, itemize your contributions and deduct these from the total amount needed.

Tip 4: Do It As A Side Hustle First[ps2id id=’Do-It-As-A-Side-Hustle-First’ target=”/]

Tip 5: Make The Jump[ps2id id=’Make-The-Jump’ target=”/]

You’re now juggling your full-time work and your side hustle. The time you originally set to achieve your big goal is fast approaching.

You’re now juggling your full-time work and your side hustle. The time you originally set to achieve your big goal is fast approaching.

1. Secure Enough Clients Beforehand

2. Have A Plan To Land More Clients

Did you know that being a solopreneur also means being a hustler?

Boom You Are In

You’ve successfully make the jump and kick start a 7 digit income business. Now you enjoy the benefits of being a boss of your own.

Tell us which of these tips works well for you and don’t forget to share this article to your colleague so that they can learn how to be the boss of their own and escape the grind of the 9 to 5 job.

Get latest articles like this sent right in your inbox.

Great content! Super high-quality! Keep it up! 🙂